Fundamentals

Fundamentals

Getting Started

Getting Started

How to Get Started in Real Estate Investing

How to Get Started in Real Estate Investing

How to Get Started in Real Estate Investing

A practical, eight-step path from your first $100 to a diversified portfolio; without becoming a landlord.

A practical, eight-step path from your first $100 to a diversified portfolio; without becoming a landlord.

A practical, eight-step path from your first $100 to a diversified portfolio; without becoming a landlord.

Omar Elghazaly

CEO, PSFnetwork

CEO, PSFnetwork

Published

Published

Published

•

•

TL;DR

Real estate investing is the practice of buying property; directly, fractionally, or through a fund to earn rental income and benefit from appreciation. As of 2026, you can start with as little as $100 on fractional platforms like PSFnetwork, $10 on REITs, or roughly $20,000–$60,000 in down payment for a direct rental. The simplest beginner path: open a fractional account, diversify across 5–10 properties, reinvest distributions for the first three years.

Real estate investing is the practice of buying property; directly, fractionally, or through a fund to earn rental income and benefit from appreciation. As of 2026, you can start with as little as $100 on fractional platforms like PSFnetwork, $10 on REITs, or roughly $20,000–$60,000 in down payment for a direct rental. The simplest beginner path: open a fractional account, diversify across 5–10 properties, reinvest distributions for the first three years.

Most beginners assume real estate investing means buying a house, finding tenants, and fixing water heaters at midnight. That model still exists — and still works — but it is no longer the only option. Over the last five years, fractional platforms, public REITs, and tokenized offerings have lowered the entry point from tens of thousands of dollars to less than a meal out.

This guide is for the reader sitting on $500 to $50,000 of investable cash who wants real estate exposure without becoming a landlord. We will walk through the four practical paths into the asset class, the eight steps from "I am curious" to "I own a piece of a duplex in Indianapolis," and the six mistakes that cost new investors the most money.

Why real estate, why now

Residential real estate has produced an inflation-adjusted return of roughly 4–6% annually over the last forty years in the United States, with materially lower volatility than equities [1]. The asset is uncorrelated enough with the S&P 500 to be a useful diversifier — and unlike most financial assets, it generates cash flow you can spend without selling the underlying.

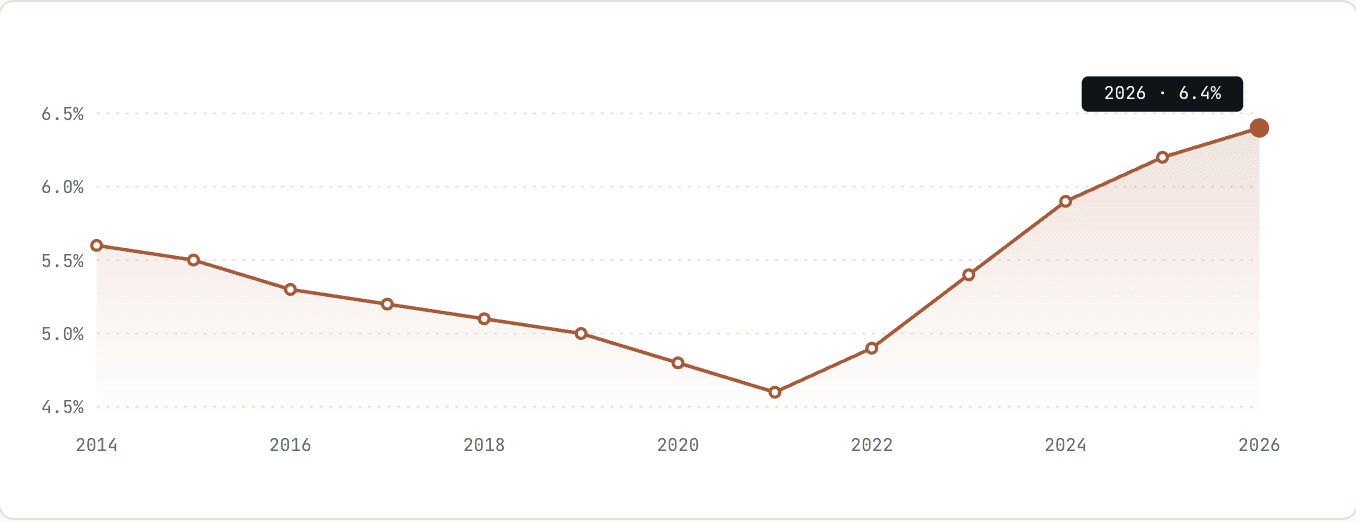

The case for starting in 2026 is mechanical, not emotional. After two years of repricing, single-family rental cap rates have widened to 6.4% on average, the highest since 2014 [2]. Fractional platforms now exist at scale — five years ago, the entire category was under $300 million in assets; today it is north of $4 billion [3].

"Buying real estate by the square foot does the same thing index funds did for stocks in the 1970s — it removes the all-or-nothing decision."

— Daniel Cho, CFA

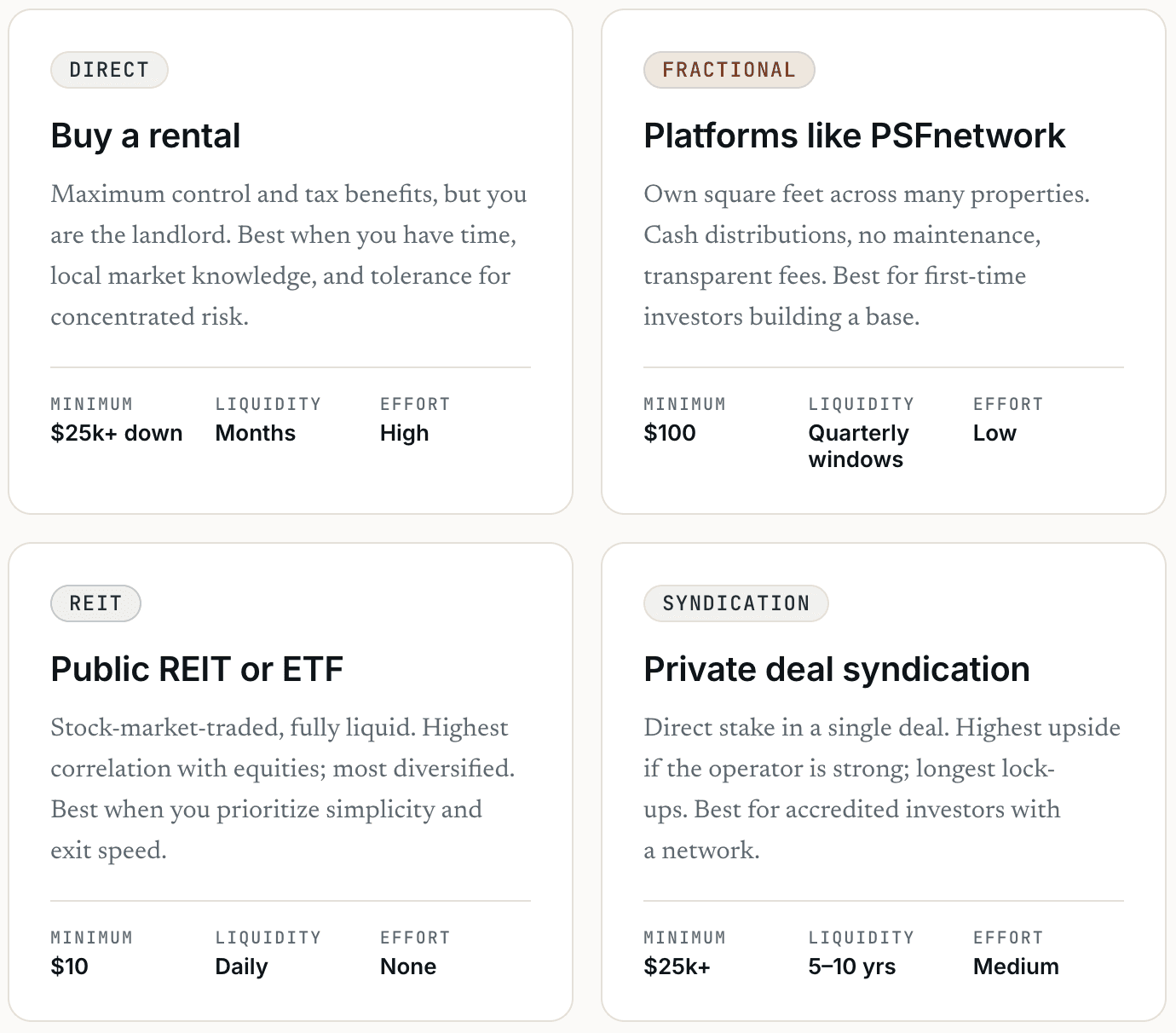

Four paths to ownership

Each path trades off control, capital, liquidity, and effort differently. There is no universal best — only the best for your situation today.

For most beginners, fractional is the highest-leverage starting point: low minimum, low effort, and the ability to spread risk across cities and property types from day one. The rest of this guide assumes that path, but the framework applies to any of them.

Eight steps to your first property

None of these steps is hard in isolation. The discipline is doing all eight, in order, before you move capital. Most failed beginner portfolios skip step 02, 04, or 05.

01 Define why you want exposure

Income, growth, inflation hedge, or all three? The answer determines property mix. Income-focused investors weight stabilized rentals; growth-focused investors weight value-add and emerging markets.

02 Set a budget you can leave alone

Real estate is illiquid. A useful rule of thumb: only commit capital you will not need for at least 36 months. Keep a separate emergency fund untouched.

03 Choose your account type

A taxable brokerage works for most. If you have self-directed IRA capacity, fractional real estate held inside an IRA defers the tax on rental distributions.

04 Verify the platform's regulation

Look for Reg A+ or Reg D filings on SEC EDGAR. Read the most recent offering circular. If the platform cannot show you a filing, it is not a real platform.

05 Diversify across 5–10 properties

Concentrating in one building defeats the point of fractional ownership. Allocate roughly equally across cities and property types — single-family, multi-family, mixed-use.

06 Set distributions to reinvest

For the first three years, compound your rent. A $1,000 starting position growing at 8% reinvested becomes $1,260 in three years; spent, it stays at $1,000.

07 Track on a quarterly cadence

Public real estate moves daily; private real estate moves slowly. Reviewing more than once a quarter creates noise without insight.

08 Add capital with a schedule, not a feeling

Pick a monthly or quarterly contribution and stick to it. Dollar-cost averaging removes the timing question and tends to outperform lump-sum investing in choppy markets.

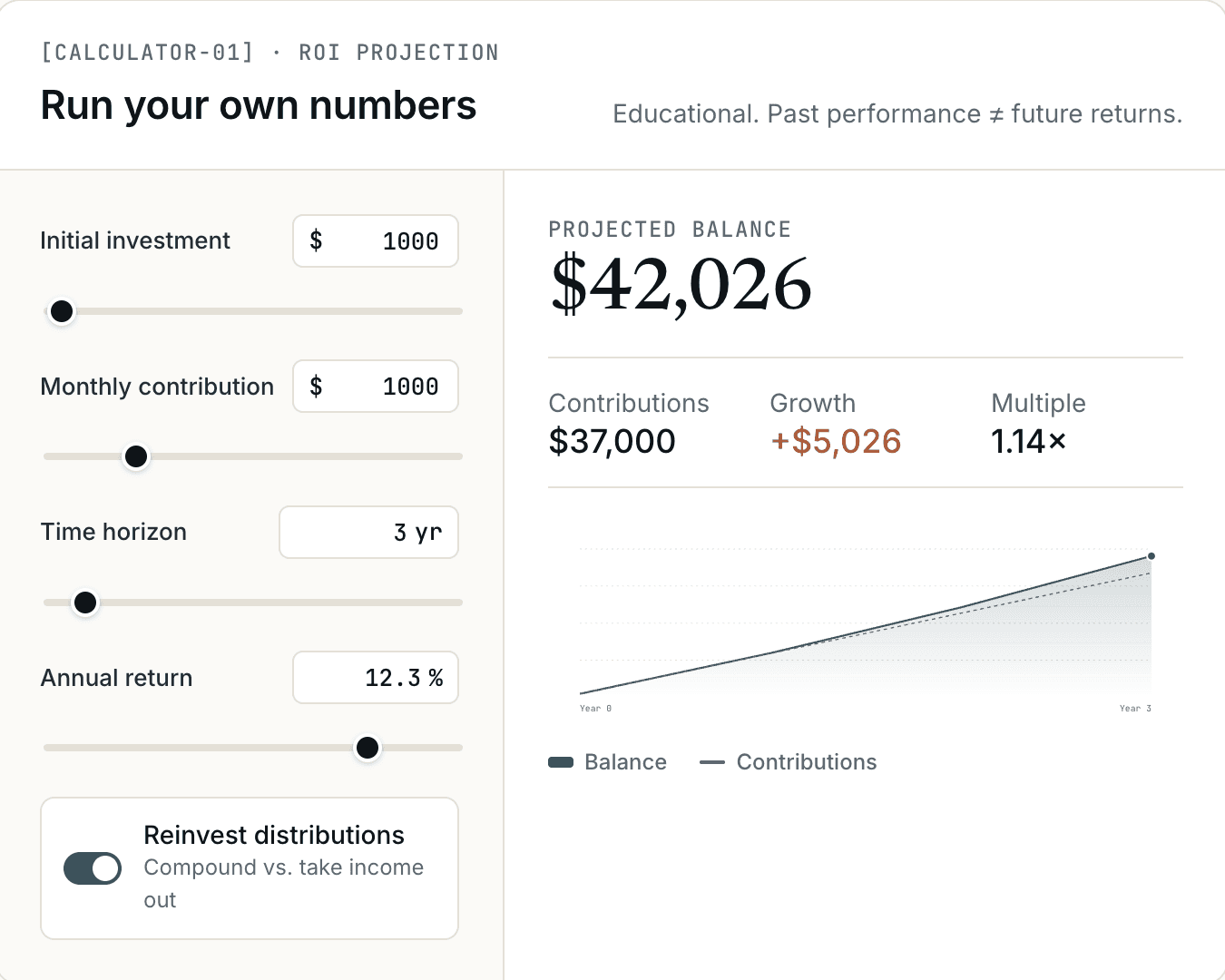

What $1,000 actually does

Real numbers help. The chart below assumes an 8% annualized return — roughly the historical average for stabilized US single-family rentals net of fees [4]. The interactive calculator lets you change every assumption.

Two observations from running these scenarios. First, monthly contributions matter more than the starting amount once you cross five years. Second, turning off "reinvest" cuts the ten-year outcome by roughly a third — a reminder that compounding is the entire game.

Six mistakes new investors make

We reviewed twelve months of platform support tickets across three fractional services to identify the most common, most costly beginner errors. Six showed up in roughly 80% of cases.

01 Concentration in one property

Buying one $5,000 stake instead of five $1,000 stakes is the single most common mistake. The whole point of fractional is diversification — use it.

02 Ignoring the offering circular

Reg A+ filings disclose every fee, conflict, and risk. Investors who skip them are surprised by 2% AUM fees that compound over a decade.

03 Treating it like a stock

Checking your portfolio daily creates anxiety without information. Property values are reassessed quarterly at most. Set a calendar reminder, then close the tab.

04 Spending the distributions

A 3% yield spent yearly compounds at 0%. The same 3% reinvested compounds with the property's appreciation.

05 Chasing yield over location

A 12% advertised yield in a tertiary market often comes with tenant turnover that wipes the yield out. A 6% yield in a stable metro usually beats it over five years.

06 Forgetting the lock-up

Most platforms restrict redemptions to quarterly windows with caps. If you might need the money in 18 months, this asset class is wrong for you.

Two observations from running these scenarios. First, monthly contributions matter more than the starting amount once you cross five years. Second, turning off "reinvest" cuts the ten-year outcome by roughly a third — a reminder that compounding is the entire game.

Most beginners assume real estate investing means buying a house, finding tenants, and fixing water heaters at midnight. That model still exists — and still works — but it is no longer the only option. Over the last five years, fractional platforms, public REITs, and tokenized offerings have lowered the entry point from tens of thousands of dollars to less than a meal out.

This guide is for the reader sitting on $500 to $50,000 of investable cash who wants real estate exposure without becoming a landlord. We will walk through the four practical paths into the asset class, the eight steps from "I am curious" to "I own a piece of a duplex in Indianapolis," and the six mistakes that cost new investors the most money.

Why real estate, why now

Residential real estate has produced an inflation-adjusted return of roughly 4–6% annually over the last forty years in the United States, with materially lower volatility than equities [1]. The asset is uncorrelated enough with the S&P 500 to be a useful diversifier — and unlike most financial assets, it generates cash flow you can spend without selling the underlying.

The case for starting in 2026 is mechanical, not emotional. After two years of repricing, single-family rental cap rates have widened to 6.4% on average, the highest since 2014 [2]. Fractional platforms now exist at scale — five years ago, the entire category was under $300 million in assets; today it is north of $4 billion [3].

"Buying real estate by the square foot does the same thing index funds did for stocks in the 1970s — it removes the all-or-nothing decision."

— Daniel Cho, CFA

Four paths to ownership

Each path trades off control, capital, liquidity, and effort differently. There is no universal best — only the best for your situation today.

For most beginners, fractional is the highest-leverage starting point: low minimum, low effort, and the ability to spread risk across cities and property types from day one. The rest of this guide assumes that path, but the framework applies to any of them.

Eight steps to your first property

None of these steps is hard in isolation. The discipline is doing all eight, in order, before you move capital. Most failed beginner portfolios skip step 02, 04, or 05.

01 Define why you want exposure

Income, growth, inflation hedge, or all three? The answer determines property mix. Income-focused investors weight stabilized rentals; growth-focused investors weight value-add and emerging markets.

02 Set a budget you can leave alone

Real estate is illiquid. A useful rule of thumb: only commit capital you will not need for at least 36 months. Keep a separate emergency fund untouched.

03 Choose your account type

A taxable brokerage works for most. If you have self-directed IRA capacity, fractional real estate held inside an IRA defers the tax on rental distributions.

04 Verify the platform's regulation

Look for Reg A+ or Reg D filings on SEC EDGAR. Read the most recent offering circular. If the platform cannot show you a filing, it is not a real platform.

05 Diversify across 5–10 properties

Concentrating in one building defeats the point of fractional ownership. Allocate roughly equally across cities and property types — single-family, multi-family, mixed-use.

06 Set distributions to reinvest

For the first three years, compound your rent. A $1,000 starting position growing at 8% reinvested becomes $1,260 in three years; spent, it stays at $1,000.

07 Track on a quarterly cadence

Public real estate moves daily; private real estate moves slowly. Reviewing more than once a quarter creates noise without insight.

08 Add capital with a schedule, not a feeling

Pick a monthly or quarterly contribution and stick to it. Dollar-cost averaging removes the timing question and tends to outperform lump-sum investing in choppy markets.

What $1,000 actually does

Real numbers help. The chart below assumes an 8% annualized return — roughly the historical average for stabilized US single-family rentals net of fees [4]. The interactive calculator lets you change every assumption.

Two observations from running these scenarios. First, monthly contributions matter more than the starting amount once you cross five years. Second, turning off "reinvest" cuts the ten-year outcome by roughly a third — a reminder that compounding is the entire game.

Six mistakes new investors make

We reviewed twelve months of platform support tickets across three fractional services to identify the most common, most costly beginner errors. Six showed up in roughly 80% of cases.

01 Concentration in one property

Buying one $5,000 stake instead of five $1,000 stakes is the single most common mistake. The whole point of fractional is diversification — use it.

02 Ignoring the offering circular

Reg A+ filings disclose every fee, conflict, and risk. Investors who skip them are surprised by 2% AUM fees that compound over a decade.

03 Treating it like a stock

Checking your portfolio daily creates anxiety without information. Property values are reassessed quarterly at most. Set a calendar reminder, then close the tab.

04 Spending the distributions

A 3% yield spent yearly compounds at 0%. The same 3% reinvested compounds with the property's appreciation.

05 Chasing yield over location

A 12% advertised yield in a tertiary market often comes with tenant turnover that wipes the yield out. A 6% yield in a stable metro usually beats it over five years.

06 Forgetting the lock-up

Most platforms restrict redemptions to quarterly windows with caps. If you might need the money in 18 months, this asset class is wrong for you.

Two observations from running these scenarios. First, monthly contributions matter more than the starting amount once you cross five years. Second, turning off "reinvest" cuts the ten-year outcome by roughly a third — a reminder that compounding is the entire game.

Disclaimer

This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Investments involve risk, including potential loss of principal. Past performance does not guarantee future returns. Investments are offered through PSFnetwork MasterSeries LLC under Reg A. Please review the offering circular and consult a qualified financial advisor before making investment decisions.

Ready When You are

Start from square one

Start from square one

Browse fractional properties across US metros. No accreditation required.

Browse fractional properties across US metros. No accreditation required.

Keep Reading

Important information

© 2026 PSFnetwork. All rights reserved.

Important information

© 2026 PSFnetwork. All rights reserved.